If you run a Canadian brokerage in 2026, you have already heard the word "AI" more times than you can count. Pitch decks, conference keynotes, LinkedIn posts. Most of it is noise. A small slice of it is the actual reason your competitors are quoting commercial accounts in hours instead of days.

This guide is the practical version of that conversation. No "AI will revolutionize insurance" framing — five concrete workflows where AI is doing real work in brokerages today, seven questions to vet a vendor before signing, and a four-week rollout plan that won't break the BMS, your team, or the client experience.

Why brokers are talking about AI in 2026

Two things changed between 2023 and 2026.

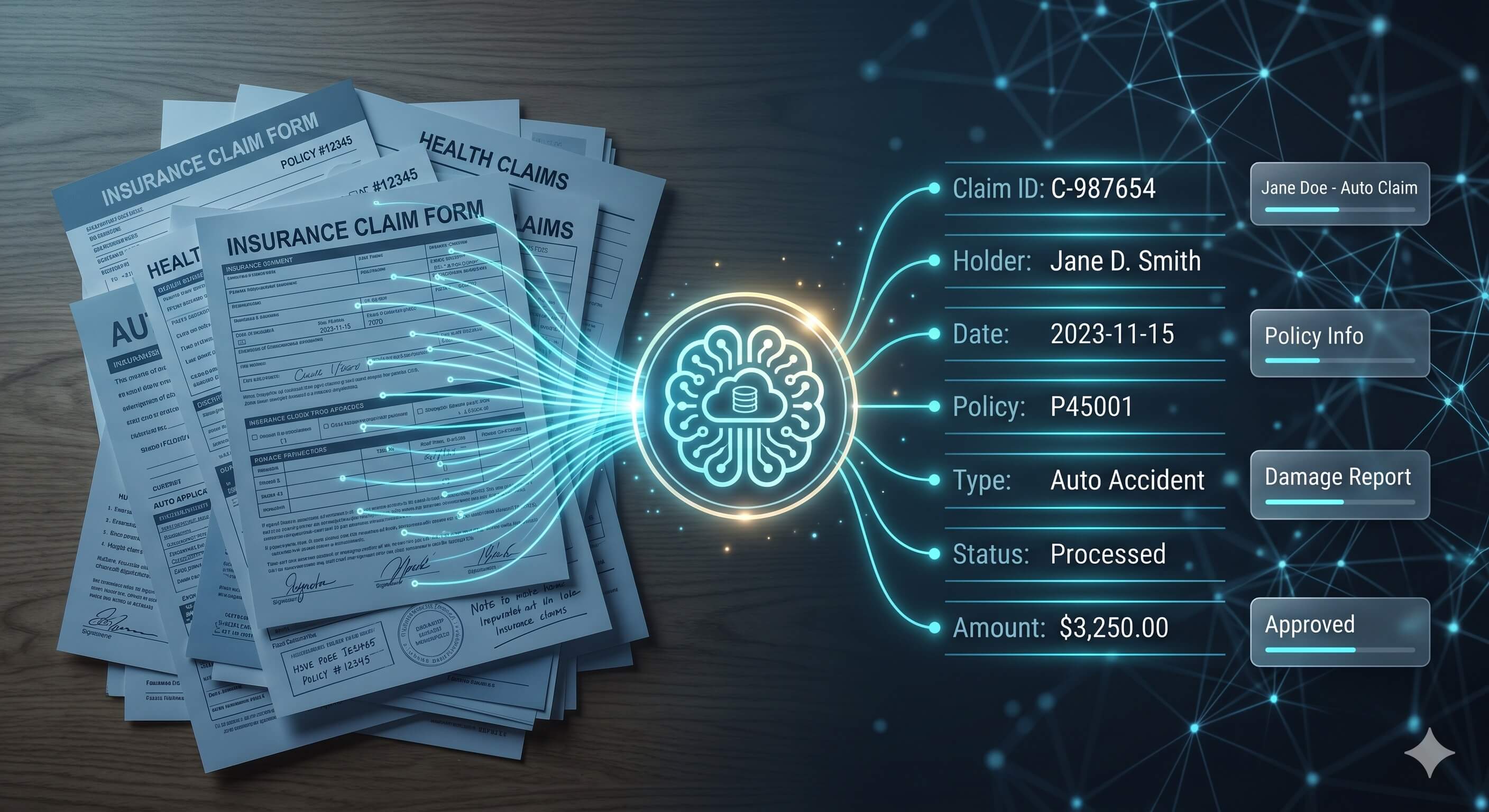

The first is technical. Generative models became cheap and accurate enough to handle structured insurance data — CSIO ACORD XML, scanned applications, multi-page commercial submissions — not just chat. Until recently, "AI for brokers" mostly meant a clever wrapper around ChatGPT. That era is over. Production-grade tools now extract a 12-page commercial submission to a clean structured record in under sixty seconds, with citations back to the source document.

The second is ecosystem. The carriers caught up. Aviva, Intact, Wawanesa, Definity and Northbridge now publish appetite guides and underwriting rules in formats that AI tools can cross-reference automatically. The result is a step change in what a single broker can place in a day.

The wedge between brokers who adopt and those who don't isn't access — every shop can buy AI tools in 2026. It's discipline: knowing where AI helps, where it doesn't, and how to roll it out without disrupting what already works.

What "AI" actually means in a brokerage workflow

When a vendor pitches "AI for brokers," they could be selling any of five very different products. Knowing which one matters because each solves a different problem and each costs a different amount.

- Extraction — pulling client, property, vehicle, and coverage data out of CSIO XML, PDFs, scanned forms, and emails. Replaces re-typing.

- Summarization — condensing a 40-page policy or carrier endorsement schedule into the three things a client actually needs to know.

- Advisory generation — producing talking points, cross-sell opportunities, and risk flags inline with each quote, citing the carrier source for each.

- Voice — handling first-touch calls, scheduling renewal conversations, leaving structured voicemails, transcribing call notes back into the BMS.

- Orchestration — moving a submission through the pipeline (quote requested → carriers contacted → responses normalized → bind documents prepared) without a broker reaching for the BMS at every step.

These are different products under one label. A summarization tool will not flag E&O exposure. A voice agent cannot extract a CSIO file. The honest truth in 2026: no single tool nails all five categories yet. The best brokerages are running two or three specialized tools that talk to each other through the BMS or a thin orchestration layer.

The 5 broker workflows where AI moves the needle

This is the part to tell your team about in the next staff meeting. Five specific workflows, ranked by ROI.

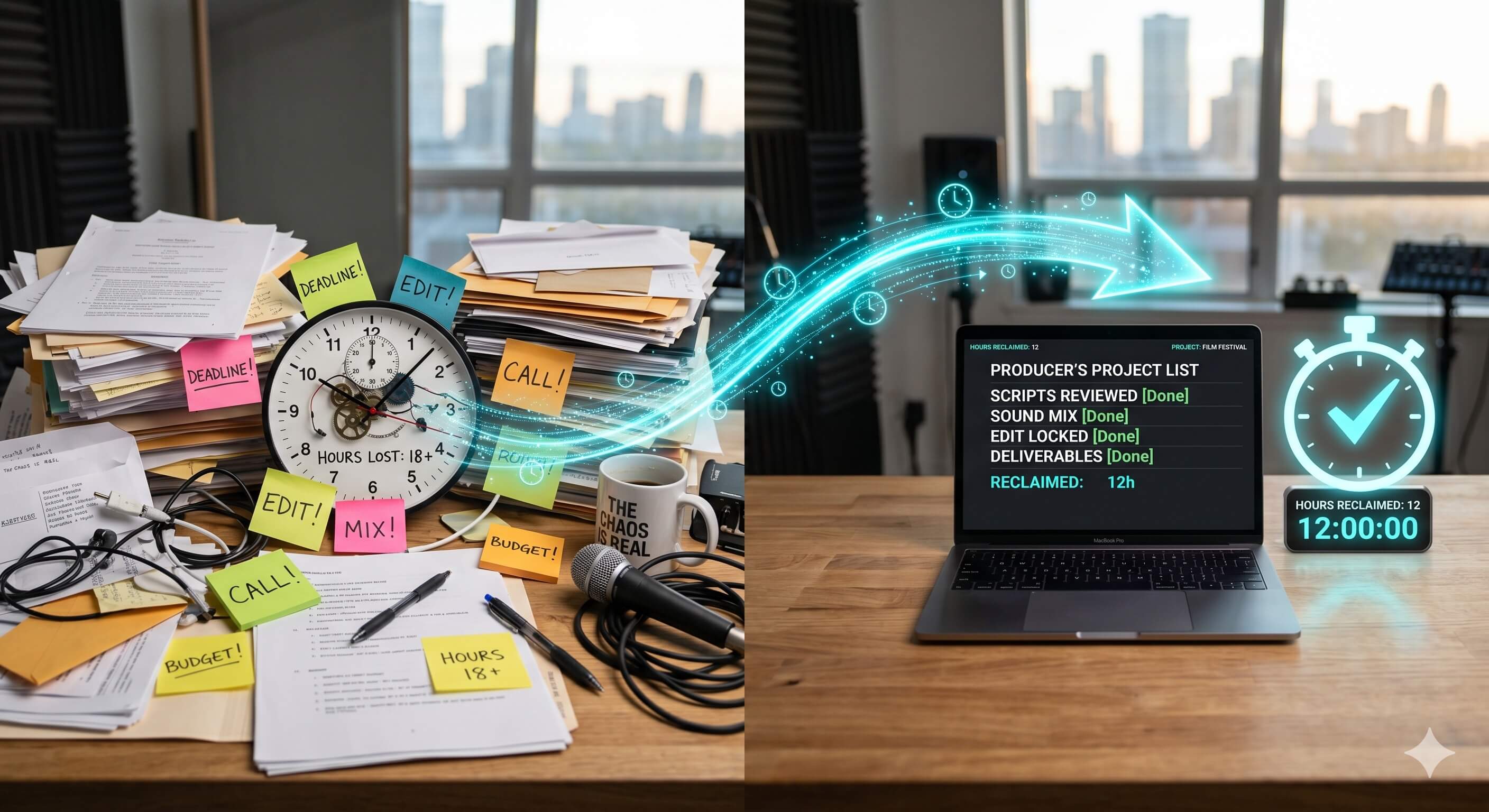

1. Submission ingestion and quoting

The workflow today: a broker receives an application or existing policy, opens the BMS, and re-keys client information, property details, coverage limits, deductibles, and prior carriers. On a clean commercial account, that's twenty minutes. On a messy one — multiple endorsements, three years of loss runs, a stack of CSIO files in different formats — it's two hours.

What AI does: extracts the entire submission to a normalized structured record in under a minute, flags discrepancies between source documents, and pre-fills the BMS. The broker reviews and corrects, instead of typing from scratch. Time saved per submission: 40-90 minutes.

2. Advisory talking points

The workflow today: a broker quotes the account, the broker writes the talking points, the broker sometimes runs out of time and emails the client a quote with no narrative. Outcome: the policy gets bound on price, not value. The broker leaves cross-sell and upsell on the table.

What AI does: generates three to five carrier-specific talking points inline with each quote, each cited against the carrier's underwriting manual or rate grid. The broker presents them verbatim or edits them in seconds. Cross-sell hit-rate goes up, time-to-bind goes down.

3. E&O risk flagging

The workflow today: the broker reads the policy, mentally checks the major exclusions, hopes nothing slipped. The good ones use a checklist. Most don't. When an E&O claim arrives two years later, the file is missing the documentation.

What AI does: scans extracted data against the carrier's appetite, identifies underinsurance, exclusions, and appetite conflicts, and tags each finding with severity and a recommended action. Critically, it writes a timestamped audit-trail entry: what was flagged, what the broker did, when. That trail is the difference between a clean E&O outcome and a hard one.

4. Renewals and remarketing

The workflow today: 90 days out, someone runs a renewal report. 60 days out, the broker emails the carrier asking for renewal terms. 30 days out, panic. 15 days out, the policy auto-renews on whatever terms the carrier offered, often with a premium increase the client never saw coming.

What AI does: monitors renewal calendars across the entire book, surfaces accounts with notable premium changes or coverage shifts at 90 days out, and pre-builds remarketing comparisons against current carrier appetites. The broker spends time only on the renewals that need attention.

5. Client communication and follow-ups

The workflow today: a broker writes the same email seven times a week — explaining a deductible, asking for a roof age, following up on a doc request. Each email costs five minutes of focused time, more if the broker is interrupted.

What AI does: drafts the email in the broker's voice, ready to review and send. Schedules and sends timed follow-ups. Transcribes voicemails into the file. The broker stays in the conversation; the typing disappears.

If you've read this far and any of the five sounds like the bottleneck in your shop, the fastest way to see it on your own data is a real demo with your real submissions.

Choosing AI tools: 7 questions every broker should ask before signing

Most AI broker tools fail one of these. Ask all seven before signing anything. Get the answers in writing.

- Where is my data stored, and is it Canadian? PIPEDA and provincial privacy regulators are not optional. Cross-border AI tools may not be a fit for commercial books with sensitive client data. Ask for the deployment region and the sub-processor list before you sign.

- Does it natively support CSIO ACORD XML — or just PDFs? PDF-only extraction is 2022 technology. ACORD-native handling is the table stakes for 2026 and the difference between accurate quoting and constant manual cleanup.

- Which carriers does it cover, and how often is the appetite data refreshed? A tool that knows Intact's underwriting rules from 2024 is dangerous, not helpful. Ask for the refresh cadence and which carriers are covered for your provinces and lines of business.

- Is there an audit trail tied to each AI suggestion? When an E&O claim hits, "the AI told us to" is not a defence. You need a timestamped record of what was suggested, what the broker did, and who approved it. Most vendors do this badly. Ask to see the audit log on day one.

- Can I bring my own model, or am I locked into the vendor's choice? Vendor-locked usually means you pay for the model layer plus a markup. BYOM saves money, gives you provider redundancy, and means you don't get stranded if the vendor's chosen model degrades.

- How does it integrate with my BMS? Applied Epic, Power Broker, Vertafore, Sigma — what's the integration mechanism? Real-time API or nightly sync? Real-time matters for advisor-on-the-call moments. Nightly sync is fine for reporting but useless during a live quote.

- What's the pricing model — per-seat, per-quote, or per-bound-policy? Per-bound aligns vendor incentives with yours. Per-seat penalizes bigger shops and means underused licenses. Per-quote can be unpredictable on volume-heavy weeks. Ask for a clear unit-economics breakdown for your expected volume.

A starter playbook: rolling out AI without disrupting the brokerage

Most AI rollouts in brokerages fail not because the tool is bad, but because the rollout is undisciplined. Run a four-week pilot before you commit a single dollar.

Week 1 — Baseline. Pick one workflow. We recommend submission ingestion because it has the most volume and the clearest before/after metric. Measure how long it takes today, broker by broker. Note error rates, rework, and where the team feels the most friction.

Week 2 — Pilot with one broker. Do not pick a junior. Pick a senior who can articulate exactly where the AI is wrong and why. Their feedback is gold; a junior's is "it's fine." Run AI side-by-side with the existing process. Don't replace yet.

Week 3 — Compare and document. Time saved? Errors? Client experience? What did the AI miss that a human caught? What did it catch that a human would have missed? Write it down. You'll need this when the conversation moves to "should we scale this to the team?"

Week 4 — Decision. Roll out to the team if the metrics check out. If not, document why and revisit in 90 days. Don't sunk-cost into a tool that doesn't fit your shop.

Four things that quietly kill AI rollouts in brokerages:

- Treating AI adoption as IT, not as a workflow change. The CIO can install the tool. Only the COO can make it succeed.

- Skipping the baseline. You can't prove ROI to your partners without one, and three months in you'll wish you had it.

- Replacing instead of augmenting. The broker job changes; it doesn't disappear. Frame the rollout that way internally.

- Buying before testing. Every reputable AI broker tool offers a 30-day pilot in 2026. If a vendor refuses, that's your answer.

What's next: where AI for insurance is heading

Today's broker tools are assistants — they generate the talking point, you decide. The next eighteen months will introduce agents that act, not just suggest. Tools that negotiate quote refinements with carrier APIs, schedule the bind call directly into your calendar, prepare the bind documents, and surface only the decisions that need a human in the loop. The infrastructure is being built right now by Anthropic, OpenAI, the major carriers, and a handful of broker-focused vendors.

What doesn't change: the broker. Insurance is a relationship business, and relationships don't scale through AI. What scales is the time the broker has for them. AI takes the repetitive sixty percent of the day so the broker can put all their judgment into the forty percent that matters — the one client who needs an advocate at renewal, the commercial account that needs a custom structure, the new prospect who came in cold and needs a real conversation.

Brokers who adopt early aren't replaced by AI. They're the ones with capacity to win the work the lagging shops can't even quote on.

FAQ

Will AI replace insurance brokers?

No. AI handles structured tasks; brokers handle judgment, relationships, and unusual risks. The shape of the job changes — fewer hours on extraction and follow-ups, more on advisory work and complex placements. The brokerages worth watching in 2026 are growing their books and their headcount at the same time, just with different role mixes.

Is AI for brokers secure enough for client data?

It can be, if you choose carefully. Look for Canadian data residency, SOC 2 Type II, role-based access, encryption at rest and in transit, and a clear audit trail. Avoid tools that train on your client data without explicit consent — that's a red line for any commercial book.

How much does AI for insurance brokers cost in 2026?

Specialized broker AI tools range from roughly $50 to $300 per seat per month, often plus a per-bind fee. Generic LLMs (ChatGPT Enterprise, Claude for Work) are cheaper but lack carrier-specific intelligence and audit trails — fine for drafting emails, not enough for quoting or risk flagging.

Will it work with my BMS?

Most modern AI broker tools integrate with Applied Epic, Power Broker, Vertafore, and Sigma. Confirm the integration mechanism — real-time API or nightly sync — and the supported entities (clients, policies, activities, attachments) before signing.

Where should I start?

Submission ingestion and quoting. It's the highest-volume, most painful workflow in most brokerages and the one with the clearest ROI inside thirty days. Once that's in place, advisory talking points and renewal monitoring are the natural follow-ons.