Most Canadian insurance brokerages grow by accident. New business comes in faster than existing business leaves, the team works harder, and at the end of the year the book is up six or seven percent. The brokerages compounding at 15-25% a year aren't working harder. They're working in a deliberate sequence.

This is that sequence — the modern playbook for growing a Canadian brokerage in 2026. Four phases, run in order, each building on the last. Skipping or reordering phases is the most common reason brokerage growth stalls.

The four phases, briefly

Phase 1 — Efficiency. Reclaim 10+ hours a week from each producer's admin time. Without this, every other phase amplifies overload.

Phase 2 — Cross-sell the book you have. Convert single-line clients to multi-line. The cheapest growth lever in any brokerage.

Phase 3 — Acquire deliberately. Build owned-attention channels (SEO, partnerships, referrals) before paid channels. Compound for years.

Phase 4 — Dominate a niche. Pick a vertical, become the unambiguous best in it, raise margins.

The order matters. A brokerage that runs Phase 3 acquisition while still bleeding 15 hours a producer per week to admin will burn out the team and watch retention drop. A brokerage that adds phase 4 niche dominance before fixing Phase 1 efficiency builds a book it can't service well. This is why growth stalls — not because the brokerage is doing the wrong things, but because it's doing them in the wrong order.

Phase 1: Efficiency (months 1-3)

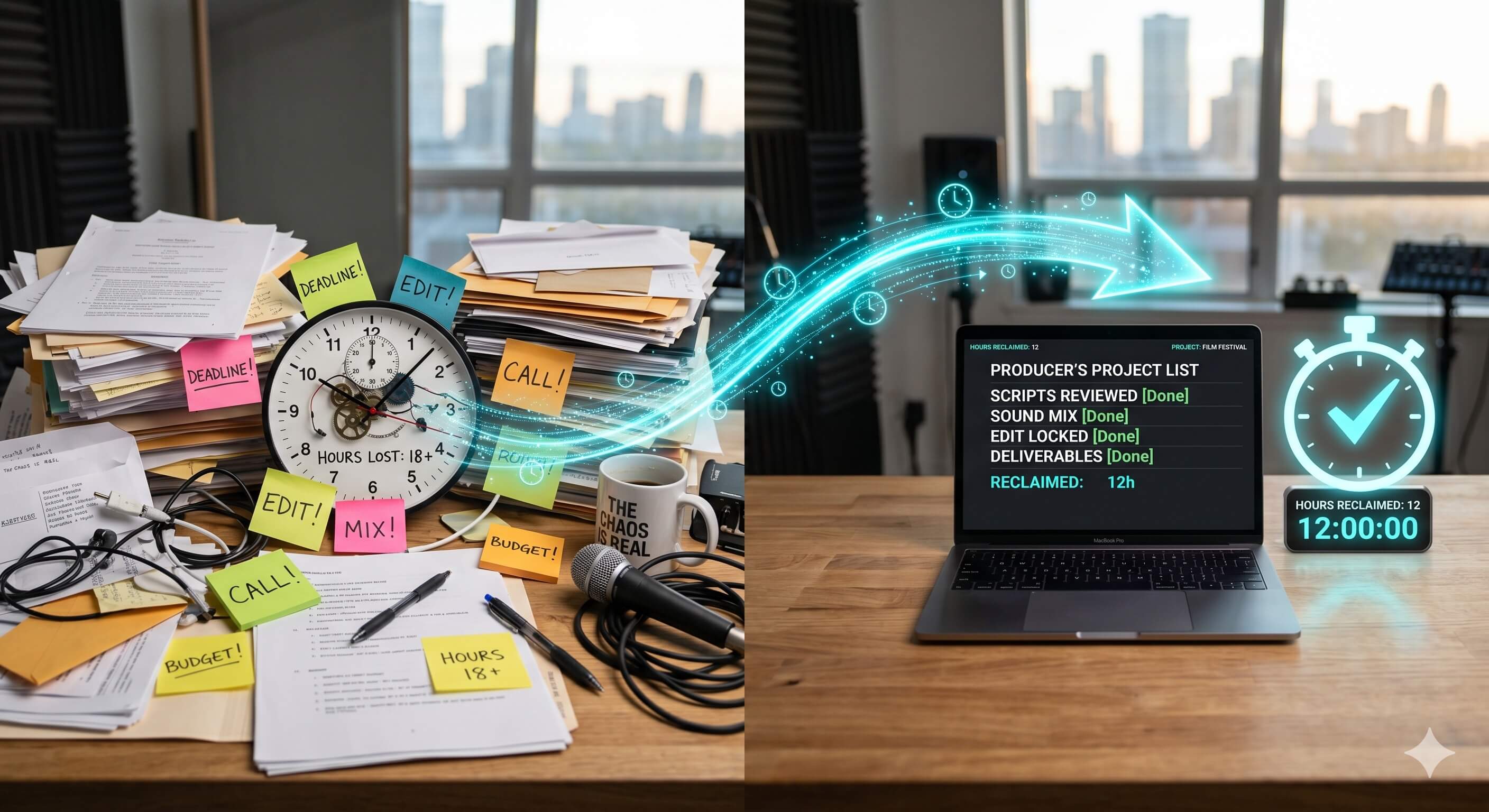

The first phase of growth is taking time off the producer's plate. A producer who's underwater on admin doesn't sell, doesn't cross-sell, doesn't return calls promptly. Phase 1 is the unglamorous foundation everything else rests on.

The actions, in priority order:

- Audit how the team's time is actually spent. Three producers, one week, five buckets (selling, servicing, quoting, admin, other). Don't skip this — every later decision references the audit.

- Run the five quick wins: standardized intake, focus blocks, single-channel document chasing, end-of-day BMS hygiene, pre-written renewal templates. These cost nothing.

- Add one AI tool — submission ingestion. This is the highest-volume admin task in most brokerages and the one with the cleanest ROI. Run a 4-week pilot before scaling.

We've covered this phase in detail in Cut 10+ Hours of Admin Per Week. The key metric to track: producer admin hours per week, before vs after. Aim for a 35-50% reduction within 90 days.

A brokerage that gets through Phase 1 has unlocked the capacity for everything that follows. A brokerage that skips it watches Phase 2 and Phase 3 fail because nobody has time to execute.

Phase 2: Cross-sell the book (months 3-6)

The second-cheapest policy a brokerage will write this year is the second policy on a client it already has. Before chasing new acquisition, the playbook says: convert single-line clients to multi-line.

The actions:

- Pull the segmentation query. Single-line clients by category (auto-only, home-only, personal-only commercial owners). Most brokerages discover 55-70% of their book is single-line.

- Train the team on the five trigger moments where cross-selling actually works: at binding, at life events, at renewal premium changes, after claim resolution, after a partner-driven introduction.

- Run a structured 60-day book-mining sprint. Pick 100 of the strongest single-line relationships. Two cross-sell asks per producer per day on triggers. Ten book-mining touches per producer per week.

We've covered this phase in detail in Cross-Selling Insurance: How to Turn One Policy Into a Multi-Line Client. The metric to track: lines per client, quarterly. A typical brokerage running this with discipline moves from 1.4 lines per client to 1.8-2.0 inside 12 months — a meaningful book-value increase with effectively zero acquisition cost.

Phase 2 is also where the brokerage's articulation of the value of independent advice gets tested. Cross-sell asks land harder when the broker can articulate why bundling with them is structurally different than buying from a direct writer.

Phase 3: Acquire deliberately (months 6-18)

With Phase 1 and Phase 2 in place — producer capacity unlocked, existing book densified — the brokerage is ready to run real acquisition. Most brokerages start here and wonder why nothing compounds. Without the prior phases, new clients overflow capacity and existing clients drift.

Phase 3 is where the channel-by-channel work happens. The right channel mix for an independent Canadian brokerage in 2026 is heavily owned-attention biased:

- Niche SEO content. Pick 2-3 niches you want to dominate. Publish one ~2,000-word post per week answering real client questions. Compounds for years.

- Partnership pipeline. 3-5 mortgage broker partners and 3-5 realtor partners (see the broker–realtor–mortgage playbook). Highest-conversion lead source available.

- Existing-client referral motion. Structured asks at binding, claims, and renewal. Track in BMS. Most brokerages double their referral rate within 6 months of running this with discipline.

- Tenant-first acquisition for younger customers. Use tenant insurance as the wedge product to acquire under-35 clients who graduate to home + auto in years 5-10.

- Google Business Profile + reviews discipline. Daily, 10 minutes. Aim for 10 new reviews per month.

- Paid search on buying-intent keywords only. Use after the organic channels are humming, never before. Bid on city + product + "quote," not on generic "insurance."

The full mechanics of each channel are covered in Marketing for Independent Insurance Brokers. The key Phase 3 metric: source-of-business attribution on every new bind. If you can't tell which channel produced last month's wins, you can't double down on what's working.

A brokerage running Phase 3 with discipline produces 15-25% net new business growth in year 1, accelerating to 30-50% in year 2 once the compounding channels (SEO, partnerships) hit scale.

Phase 4: Niche dominance (year 2 onwards)

The fourth phase is where margin expansion lives. A brokerage that's the clear best in its city for "contractors with 5-50 employees" or "restaurants under $5M revenue" or "high-net-worth families with secondary properties" charges differently, retains differently, and competes on something other than price.

Phase 4 actions:

- Pick the niche. Not three niches — one. The brokerage you're trying to be in 5 years has one signature niche. Personal lines + commercial + benefits is not a niche; "the contractor brokerage in Calgary" is.

- Reorient marketing. Niche SEO content compounds harder when it's about one specific vertical. Niche partnerships go deeper. Niche reviews and case studies build authority other shops can't replicate.

- Reorient the team. Senior producers in the niche get paid for niche expertise, not generalist breadth. New hires are interviewed for niche fit. The brokerage's reputation in the niche becomes the recruiting tool.

- Reorient the carrier mix. Carriers respond to brokerages with concentrated niche books. Better appetite, better pricing, sometimes exclusive products. This is the margin expansion moment.

A brokerage that successfully runs Phase 4 in years 2-5 typically sees:

- New business close rate in the niche 3-5x its general book

- Retention in the niche book 10-15 percentage points higher

- Average premium per client 30-60% higher

- Margins improving year over year as carrier relationships deepen

We cover the full niche-dominance playbook in Niching Down: Why Specializing in One Vertical Wins More Business in 2026.

What separates the compounders from the strugglers

Three patterns show up consistently in the brokerages compounding at 15-25% a year vs the ones stuck at 3-5%:

They run the phases in order. They don't try to acquire while bleeding admin hours. They don't niche before they've cross-sold. The discipline of sequencing is itself the competitive advantage.

They measure ruthlessly. Lines per client, source of business, producer admin hours, niche bind rate, renewal retention by cohort. Numbers reviewed monthly, not annually. Strugglers measure annually and discover problems too late to fix.

They invest in producer capacity, not headcount. A 6-broker shop that runs the four phases well outperforms a 10-broker shop running on the old playbook. Capacity comes from process and tools; headcount is a lagging indicator.

The hard market context (and why this playbook still works)

Canadian property insurance is in a hardening market in 2026. Premiums are up, capacity is constrained on certain risks, and clients are price-shocked. None of this changes the playbook — it just sharpens its importance.

In a hard market:

- Phase 1 efficiency matters more, because remarketing volume is up and producer capacity is tighter.

- Phase 2 cross-selling matters more, because the easiest way to retain a price-shocked client is to deepen the relationship across multiple lines.

- Phase 3 acquisition is harder via paid channels (everyone is competing for the same clicks) but easier via partnerships (clients are actively looking for advisors).

- Phase 4 niche dominance is the strongest defence — niche carriers maintain capacity in niches they prioritize even when general capacity tightens.

For the renewal-time tactics specific to a hard market, see Hard Market Survival: Negotiating Renewals When Premiums Spike.

What we've stopped recommending in 2026

Three things that were standard broker-growth advice five years ago and no longer make sense:

- Generic content marketing. "Why insurance is important" articles produce zero business. Niche, long-tail SEO content does.

- Heavy paid social spend. Algorithmic reach for unboosted broker pages is effectively zero, and broad social ads waste budget. Localized, narrow-targeted ads with a specific product offer can still work.

- Mass-market sponsorships. The local arena banner, the Chamber gala, the United Way table. Awareness without intent. Spend the budget on partnerships and reviews.

A 12-month operating cadence

For brokerages that want a calendar, this is the rhythm we'd recommend:

- Q1. Phase 1 audit and quick wins. AI submission-ingestion pilot.

- Q2. Phase 2 cross-sell sprint. Lines per client up by 0.2-0.4.

- Q3. Phase 3 launch. Partnership pipeline + niche SEO + GBP discipline. First 3-5 partnerships in motion.

- Q4. Continue Phase 3. Begin Phase 4 niche selection conversation. Carrier-mix review.

Year 2 starts with Phase 4 commitment and the disciplines from years 1 continuing. By year 3, niche dominance is the dominant theme; the prior phases are running on autopilot.

FAQ

What if our brokerage is already past Phase 1?

Great — but verify with an audit anyway. Most brokerages think they're past Phase 1 and aren't. The audit takes a week and either confirms readiness for Phase 2 or surfaces hidden bleed.

Can we run Phase 2 and Phase 3 simultaneously?

Light overlap is fine in months 5-6 — start the partnership conversations while finishing the cross-sell sprint. Full Phase 3 launch should wait until Phase 2's discipline is sticky.

Does this playbook work for a 2-producer shop?

Mostly yes, with adaptations. Smaller shops compress the timeline (each phase is shorter because the volume is lower) and rely more on the owner's personal partnership relationships in Phase 3.

When do we hire?

Hire after capacity is unlocked, not before. Adding a producer to a brokerage that's still bleeding admin hours just adds an underperforming producer. Phase 1 efficiency is the prerequisite to a productive hire.

What's the single highest-leverage decision?

Picking the niche in Phase 4. The right niche compounds for a decade; the wrong one stalls everything. Spend serious time on this — interview clients in the candidate niches, validate carrier appetite, look at competitor density.